Underinsurance Claims Scenario

You wouldn’t want to hear that your insurance won’t be enough to cover a claim. Businesses across the UK that are already struggling, thanks to surging inflation and its knock-on effect on

Underinsurance & what it means to your business

What is underinsurance? Your insurance premium is calculated based on your individual circumstances and the amount of cover you choose to take out to protect your business. Underinsurance occurs when you’ve not

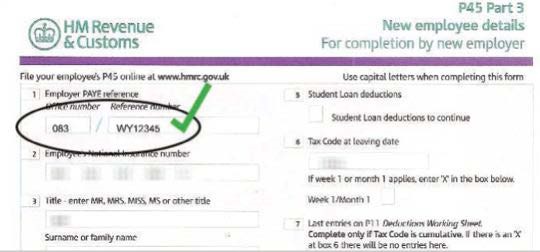

Employer Reference Numbers for ELTO requirements

What is an ERN? The Employer Reference Number (ERN), also known as the Employer ‘Pay As You Earn’ (PAYE) reference, is a unique combination of letters and numbers that HMRC uses to

Why consider Employment Practices Liability cover?

The complex nature of employment laws means that companies need to keep up to date with changes to legislation and regularly review and update internal procedures. For businesses of any size, employment